PoP: China & The Xi Agenda

A Look at China under President Xi

TOPIC: CHINA & THE XI AGENDA

Through the lens of the Pillars of Power, we take a look at China under President Xi – with a particular focus on his agenda and what has come of it thus far.

This is not meant to be a comprehensive coverage of every policy, but rather a high level overview of primary areas – along with a connection of the dots across them.

These initiatives and events have been spaced over a decade, so it’s often (purposefully) difficult to keep track and tie the cause to the (lagged) effect. For years no one noticed China’s rising strength – similar to the analogy of the frog in the pot with warm, but rising water temperature. Today it is fairly obvious that the water is boiling.

TECHNOLOGY

Since President Xi took office in 2013, he set out with an ambitious plan that spanned decades – a little different than the West, where the election process essentially forces shorter time horizon decision-making (topic for another day). With time on his side Xi laid out a vision, intermittently cracked down on opposition and corruption to (attempt to) increase control and fix the foundation, and funneled money and resources to key areas to execute. While there have been a few stages, Technology has always been a core focus – particularly as it relates to Manufacturing.

A (very) brief history. China began its ascent as the primary manufacturing plant for the world back in the ‘90s, with a material acceleration in 2001 upon entering the WTO. They started with labor-intensive, low value ‘trinkets,’ and over time moved up the complexity and value curves – primarily via Technological investment. Enter Made in China 2025.

Released in 2015, the Made in China 2025 ‘modern industrial’ plan is effectively a summary of Xi’s Technological ambitions. The underlying focus was on using Technology to improve their manufacturing processes (think robots) to move up the value curve and increase their competitive edge as the World’s Industrial Plant. Simultaneously they set out to increase control over those enabling Technological stacks – i.e., the inputs and supply chains to make the key Technologies (think Semiconductors). All with the end goal of dominating industries deemed strategic, namely: Information Technology (AI), Robotics, Green Energy & Vehicles, Aerospace Equipment, Ocean Engineering & Ships, Railway Equipment, Power Equipment, Agriculture Equipment, Medicine & Devices, and New Materials.

Looking at the manufacturing trend, it’s been on a one-way path higher since ~1994, with a non-linear shift up after 2001.

And looking at the industries, China is a or the leader in several on that list; to name a few:

BYD – similar to Tesla

CATL – similar to Panasonic

Huawei – similar to Apple + networking

SMIC – similar to TSMC

DeepSeek – similar to OpenAI

TikTok – similar to Meta

Alibaba – similar to Amazon

COMAC – similar to Boeing

And so on...

It’s pretty astonishing the price differential between Chinese companies and their respective Western counterparts – e.g., BYD entry-level car $10-15K; Tesla closer to ~$40K. China leads in areas across manufacturing – from EVs to Smartphones to Drones and Robots. They lead in Ship Building and High Speed Rail. They lead in Battery Technologies and Solar. Fairly obvious the dual-use cases here. And as we’ve stated before, Military power comes downstream of Technology – which we are seeing even more clearly with China’s hypersonic missiles, robots and drones.

But you also need end markets to sell those manufactured goods into – notably when your domestic demographic picture is an inverted pyramid that gets worse by the day (i.e., more elderly than working age population). And, among other things, you need a way to gain access to key resources not found domestically. Enter the Belt and Road Initiative.

Launched in 2013, the Belt and Road Initiative was pitched as a global infrastructure development strategy “to construct a unified large market and make full use of both international and domestic markets, through cultural exchange and integration, to enhance mutual understanding and trust of member nations, resulting in an innovative pattern of capital inflows, talent pools, and technology databases.” Basically they wanted to build out a trade network, find ‘physical’ outlets for excess cash (from selling goods), and ultimately increase their spheres of influence.

Looking at the results, they’ve done a decent job...

And along the way, Xi cracked down on dissenters, ultra-wealthy, and corruption to solidify his Power – most notably, the Technology crackdowns in 2018 (focused primarily on Media) followed by an even bigger one beginning in late 2020 (focused primarily on Big Tech). All of this was a bid to maintain and extend control – understanding the far-reaching powers of Technology and Money. And to make sure all parties are fully aligned with his Total National Security Paradigm – “a national security system that integrates such elements as political, military, economic, cultural, social, science and technology, information, ecological, resource, and nuclear security.”

After years of suppression, last week Xi just hosted all of the most important Chinese Technology leaders at the Private Enterprise Symposium – symbolizing the re-endorsement of Technology and wealth accumulation by the State (Alibaba’s stock price – down ~80% during the crackdowns; already up over 75% this year). And after years of subtle under-the-radar progress, in the last ~2 years Chinese companies have begun celebrating their success and Power posturing – notably with the Huawei 7nm chip release (during US Secretary of Commerce Raimondo’s China visit), BYD’s accelerated global expansion, and the latest DeepSeek R1 release (on Trump’s inauguration day). The signal is clear: Xi is no longer afraid to challenge the US out in the open.

The progress is indisputable; however, a key Technology bottleneck still remains: Semiconductors. Semiconductors are the key to self-sufficiency and full control over the Technological stack – the base layer or key enabling Technology for this AI Revolution. China has spent over a decade building up its domestic Semiconductor supply chain – a key component of the Made in China 2025 plan – with the goal of full self-sufficiency (i.e., removing Western dependence). They attempted to accelerate these plans by acquiring many Western Semiconductor companies with surprisingly no US pushback – asleep at the wheel? profiting/misaligned incentives? National Security not a consideration? – until Trump came in in 2016 (shutting down Chinese M&A, among other areas). Despite these clear initiatives and Global M&A, China is still not-quite-there on leading-edge (i.e., the latest) Semiconductor chip design and/or manufacturing technologies – which are critical for building leading AI infrastructure and applications. They certainly have capabilities on lagging-edge (i.e., older, less efficient; we’ll do a piece focused on Semiconductors to explain some of this jargon). And while the Huawei 7nm chip is a sign they are catching up, mass-production of leading-edge chips has remained elusive. Part of it is the built up process know-how that compounds over time – after ~30 years, TSMC overtook Intel a few years ago in leading-edge scaling (i.e., faster, more efficient chip) and now manufactures ~90% of leading-edge semiconductors (if you want a new iPhone, you need TSMC). This all culminates in the geopolitical importance of TSMC, as well as the Western Semiconductor Capital Equipment companies that supply TSMC with the machines they need to produce the chips that enable AI.

In the meantime, because of this deficiency, China has been significantly (over) ordering Semiconductor Capital Equipment as well as leading-edge Semiconductors (notably, Nvidia GPUs manufactured at the latest node). While the US/Western administrations have had some restrictions and export controls over the last several years, none were ‘strict’ or enforced strongly enough to stop the stockpiling – until the latest batch issued in January (and effective in April). Watching what comes next will be key.

Given this backdrop and ongoing Global Power struggle, it becomes a bit more obvious why we’ve seen certain restrictive actions in the West: the banning of Huawei and ZTE smartphones and infrastructure, the banning of TikTok, the banning of BYD and Chinese cars. The list goes on. And, in fact, this whole China ‘crackdown’ initiative all began under Trump’s first administration (and continued under Biden) – as they ‘woke up’ to Xi’s plans laid out above.

This is not meant to endorse restrictions (topic for another time is creative win/win solutions), but rather recognize why – it’s pretty clear the National Security and relative Power balance underpinnings. And it should also be noted that China essentially does not allow any Western companies to operate in China unless via a local JV (think legacy automakers like GM) or after significant investment endorsed by the State (think Tesla and Apple). And even then, Xi has significantly ramped up efforts pushing domestic consumers to buy local, Chinese company products over Western counterparts (e.g., BYD over Tesla). Meanwhile, Meta, Netflix, Amazon, and the like are not allowed in China. They know the Power of Technology and the control it enables.

Ultimately, the US, as well as China and Russia, believe leadership in AI will determine the relative Power balance in the emerging Global World Order. Putin actually gave a speech about it in 2017 – “Artificial intelligence is the future, not only for Russia, but for all humankind… It comes with colossal opportunities, but also threats that are difficult to predict. Whoever becomes the leader in this sphere will become the ruler of the world.”

And as outlined above, to control and lead in AI, you must control and lead across the full Technology stack, notably the foundational building-block technologies (e.g., leading-edge Semiconductors). Even with all of this, you still need the ‘base energy layer’ to power it…

ENERGY

Energy is critical to scale and consistently power AI. And China is a net energy importer – a dependency and an area they do not fully control; a key pain point for a population of 1.4 billion. While they are not energy independent, they are also not dumb. They have been building out a comprehensive Energy strategy over the last decade…

Starting with growing closer to the country they share a 2,600+ mile border with – Russia. Russia is an energy and commodity powerhouse and a relatively valuable end market for goods. China is a manufacturing powerhouse with relative overproduction for domestic purposes. A complementary match that the two leaders recognize (Xi to Putin in 2023) – “Right now there are changes – the likes of which we haven’t seen for 100 years – and we are the ones driving these changes together.”

Domestically, China has a multi-pronged approach to Energy security. Short-term, they are highly reliant upon coal. They have minimal oil and gas reserves and have not had much success with shale. Medium-term, they are massively ramping up their nuclear capacity – ignoring the demonizing campaign against it, and embracing its relative safety, stability, density, and cleanliness. And long-term, they are the leaders in both solar and battery technologies – products of the Made in China 2025 initiative – which have already begun paying dividends.

On the more speculative front, they continue to explore new frontiers – from the Arctic with Russia (Energy resources and more efficient trading lanes as ice melts), to nuclear fusion, to space-based solar, to deep-Earth energy drilling. Many of these initiatives are picking up speed – further highlighting the importance of both the Arctic and Space (future topics) – and represent nonlinear Energy supply opportunities enabled by Technology.

Overall, pair the above with their Belt and Road Initiative and you can see how they are gradually reducing their dependence on others for Energy. But how to pay for it all…

MONEY

Control of Money is critical – notably the ability to print the currency in which you have outstanding debts. As part of the Unipolar World, the US provided Global trade security (i.e., shipping lane security, notably for Energy) and the World traded in US Dollars (USD) – the Global Reserve Currency, paired with US Treasuries as the Global Reserve Asset. President Xi did not like this dependency – trading and operating in a currency he could not print.

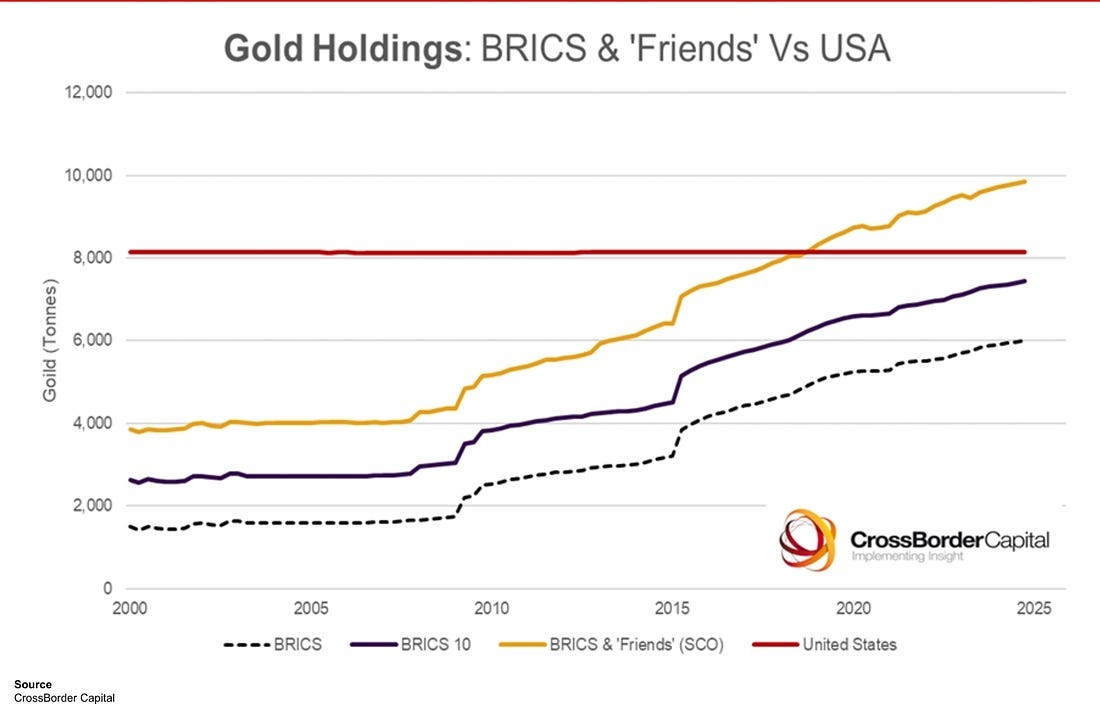

First, he stopped buying US Treasuries with US Dollars received for goods they sold – instead funneling those USDs into the Made in China 2025 and Belt and Road Initiatives, along with gold and commodities. This gold buying only further accelerated with the US’s freezing of Russian reserves in 2022.

Then, he began trading outside of the USD-based system with key partners – most notably its Energy providers, trading with Russia and Saudi Arabia directly using yuan, China’s printable currency. Allowing China to actually benefit from sanctioned Russian and Iranian oil – getting it on the cheap ‘outside’ the system.

Finally, the BRICS countries – spearheaded by China and Russia – have been developing an alternative currency system for years, attempting to remove their dependence on the US Dollar. And once again, highlighting the Power of controlling the base layer – Money.

All the while China under Xi has enacted strict capital controls (i.e., restricting Money outflows to avoid capital flight), kept its currency relative to the US Dollar suppressed (i.e., cheap to make their goods exports cheap), and has cracked down on anyone becoming ‘too wealthy’ (and thus Powerful). Xi’s launch of the digital RMB — a centralized Central Bank Digital Currency — further highlights how he is using Technology to increase and exert control.

Overall, the Multipolar system has begun to emerge. As highlighted by the above trade map, China’s relative influence in World trade has dramatically grown. And while prior administrations in the West have been more lax, the Trump administration has come out swinging with tariffs and the like to rebalance Global trade – all at a time when China is teetering on a deflationary crisis, partially due to its real estate bubble popping (most Chinese citizens hold wealth in real estate). We believe a likely Global Monetary event is coming later this year – likely Mar-a-Lago Accord (upcoming piece) – that will have far-reaching implications for the World Order ahead.

CONFLUENCE

We are at a tipping point in the Global World Order. With all of its Pillars of Power on the relative rise over the last decade, China is becoming more comfortable challenging the US and its Unipolar hegemony. Given its poor Demographic outlook and Debt picture, China needs to expand and grow now – which Xi has laid out in his vision for the World, and you are seeing it manifest in areas like EVs (China recently became the top Auto exporter in the World).

Overall, China has unequivocally risen as a formidable Global Power – partially as a result of Xi’s relentless focus on strengthening China’s Pillars of Power. Weak points remain – from leading-edge Semiconductors to Energy dependence to the Debt and Demographic situation – but seeing the full picture as it is is critical for assessing what is likely next. On the margin, China needs to shift its balance more toward Consumption, while the US needs to shift its balance more toward Production – a peaceful, non-zero sum outcome would be ideal. The more we can observe what is actually happening, understand why, and listen to each Party’s perspective, the more likely a creative win-win situation arises.

Once again, this is not meant to be political. It’s meant to be a realistic observation of what is actually happening. And a Framework to prepare for what might happen and most importantly – why. The Pillars of Power lay at the foundation of decisions made by people in (or seeking) Power around the World.

Thanks for reading. If it was useful, share it. If it could be more useful – let me know how (info@aquavisadvisors.com). If you have any questions, comments, or want some resource suggestions to learn more – let me know.

Change your mindset – scarcity to growth. Let’s build a positive-sum world of abundance.

Order your Mind. Harness your Money. Shape your Future.

If you still think Semiconductors (notably leading-edge, like Nvidia GPUs) are not critical to National Security -- laying the Foundation for the Technology Pillar -- then wake up.

Check out this WSJ article talking about how Chinese AI companies have been circumventing US chip restrictions (https://www.wsj.com/tech/china-ai-chip-curb-suitcases-7c47dab1?reflink=desktopwebshare_permalink)

China further doubling down on Production - notably of Critical Products.

Not surprising at all - particularly the Semiconductor side - as they look to reduce external dependencies

https://www.semafor.com/article/05/26/2025/beijing-reportedly-mulling-made-in-china-2035